Strategic depreciation choices in property renovation pay off for investors

First published 23 January 2025

Renovation offers investors a chance to boost property value and improve cash flow with strategic depreciation planning. When working with clients, accountants typically focus on broader financial aspects rather than the intricate details of plant and equipment assets, their lifespans, or depreciation rates. This is where the specialised knowledge of a quantity surveyor becomes highly beneficial.

Key take-out

Learn how strategic renovation choices can optimise cash flow for investors. Discover the impact of different depreciation methods on tax deductions and find out how accountants can assist clients in making informed decisions.

A specialist quantity surveyor prepares a comprehensive tax depreciation schedule after a renovation project but can also offer investors tailored information beforehand.

This information can help an investor to select new assets that align with their investment objectives, whether they prioritise immediate tax deductions or long-term benefits.

In this article, we examine the hypothetical case of Lisa, an investor with a long-term investment plan, who undertook a renovation project on her investment property. As Lisa embarked on this endeavour, she began to understand the crucial significance of depreciation planning in maximising cash flow and bolstering her investment strategy.

Case study

Meet Lisa, a property investor. As part of her long-term retirement plan, Lisa bought an investment property for $720,000 last year. It was originally built in 1995. With her sights set on long-term financial security, Lisa recently undertook a renovation project on the property.

Lisa’s investment strategy was to:

- renovate for growth

- hold the property for the long term

- claim tax deductions for as long as possible

With these goals in mind, she approached the renovation process with a strategic mindset, seeking guidance from professionals to ensure she made informed decisions every step of the way.

Lisa’s accountant advised her that Division 40 (plant and equipment) assets with similar functions can have varying effective lives and rates of depreciation, and that this would impact the deductions that she was entitled to.

As part of the renovation, Lisa replaced the flooring, window coverings, air conditioning and rainwater tank. The renovation presented Lisa with a myriad of choices, from selecting materials and designs to deciding on the most tax-efficient depreciation method for her newly installed plant and equipment assets.

In addition, Lisa would also be able to claim scrapping, which involves removing and disposing of any potentially depreciable asset from an investment property during the renovation process. When these older assets, such as carpets and hot water systems, are replaced or scrapped, property owners may be eligible to claim them as a tax deduction based on their remaining depreciable value.

Lisa’s accountant also alerted her to low-value pooling, which is a method of depreciating plant and equipment items at a higher rate to maximise deductions. Low-cost assets with an initial value below $1,000, as well as low-value assets initially purchased for more than $1,000 but depreciated to under $1,000 after the first year, would be included in the low-value asset pool.

Aware that these decisions could significantly impact her bottom line, Lisa’s accountant guided her towards BMT Tax Depreciation before undertaking the renovation of her property. BMT gave Lisa information to help her carefully select assets based on their effective lives, ensuring that Lisa was aware of their impact on depreciation deductions.

Lisa was faced with choosing between carpet or floating timber flooring, curtains or blinds, split system or packaged air conditioning, and a polyethylene or galvanised steel rainwater tank. These assets perform the same function but have different effective lives (Table 1).

Table 1. These assets have similar functions, but different effective lives

| Asset | Effective Life |

| Carpet | 8 years |

| Floating timber floors | 15 years |

| Blinds | 10 years |

| Curtains | 6 years |

| Split system A/C | 10 years |

| Polyethylene rainwater tank | 15 years |

| Galvanised rainwater tank | 25 years |

Lisa carefully evaluated her options, prioritising assets with longer effective lives to prolong her tax benefits and minimise the need to replace them. Below we have compared the various assets and the depreciation deductions available over their effective lives calculated using both the diminishing value and prime cost methods.

Table 2. Flooring $6,600 worth of carpet and flooring generate the following deductions over time

| Carpet or floating timber floorboards | ||||

| $6,600 worth of carpet and flooring generate the following deductions over time | ||||

| Carpet DV | Carpet PC | Floating timber DV | Floating timber PC | |

| 1 Year | $1,650 | $825 | $880 | $440 |

| 2 Year | $1,238 | $825 | $763 | $440 |

| 3 Year | $928 | $825 | $661 | $440 |

| 4 Year | $696 | $825 | $573 | $440 |

| 5 Year | $522 | $825 | $496 | $440 |

| 6 Year | $392 | $825 | $430 | $440 |

| 7 Year | $294 | $825 | $373 | $440 |

| 8 Year | $220 | $825 | $323 | $440 |

| 9 Year | $165 | - | $280 | $440 |

| 10 Year | $124 | - | $243 | $440 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 3. Window Covering curtains and blinds costing $2,550 generate the following deductions over time

| Curtains or blinds | ||||

| Curtains and blinds costing $2,550 generate the following deductions over time | ||||

| Curtains DV | Curtains PC | Blinds DV | Blinds PC | |

| 1 Year | $850 | $425 | $510 | $225 |

| 2 Year | $567 | $425 | $408 | $225 |

| 3 Year | $378 | $425 | $325 | $225 |

| 4 Year | $252 | $425 | $261 | $225 |

| 5 Year | $168 | $425 | $209 | $225 |

| 6 Year | $112 | $425 | $167 | $225 |

| 7 Year | $74 | - | $134 | $225 |

| 8 Year | $50 | - | $107 | $225 |

| 9 Year | $33 | - | $86 | $225 |

| 10 Year | $22 | - | $68 | $225 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 4. Water Tank polyethylene and galvanised water tanks costing $3,150 generate the following deductions over time

| Polyethylene or galvanised water tank | ||||

| Polyethylene and galvanised water tanks costing $3,150 generate the following deductions over time |

||||

| Polyethylene DV | Polyethylene PC | Galvanised DV | Galvanised PC | |

| 1 Year | $420 | $210 | $252 | $126 |

| 2 Year | $364 | $210 | $232 | $126 |

| 3 Year | $315 | $210 | $213 | $126 |

| 4 Year | $273 | $210 | $196 | $126 |

| 5 Year | $237 | $210 | $181 | $126 |

| 6 Year | $205 | $210 | $166 | $126 |

| 7 Year | $178 | $210 | $153 | $126 |

| 8 Year | $154 | $210 | $141 | $126 |

| 9 Year | $134 | $210 | $129 | $126 |

| 10 Year | $116 | $210 | $119 | $126 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 5. Air Conditioning split system and packaged air conditioning units costing $11,400 generate the following deductions over time

| Split system or packaged air conditioning | ||||

| Split system and packaged air conditioning units costing $11,400 generate the following deductions over time |

||||

| Split system DV | Split system PC | Packaged DV | Packaged PC | |

| 1 Year | $2,280 | $1,140 | $1,520 | $760 |

| 2 Year | $1,824 | $1,140 | $1,317 | $760 |

| 3 Year | $1,459 | $1,140 | $1,142 | $760 |

| 4 Year | $1,167 | $1,140 | $989 | $760 |

| 5 Year | $934 | $1,140 | $858 | $760 |

| 6 Year | $747 | $1,140 | $743 | $760 |

| 7 Year | $598 | $1,140 | $644 | $760 |

| 8 Year | $478 | $1,140 | $558 | $760 |

| 9 Year | $383 | $1,140 | $484 | $760 |

| 10 Year | $306 | $1,140 | $419 | $760 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 2. Flooring $6,600 worth of carpet and flooring generate the following deductions over time

| Carpet or floating timber floorboards | ||||

| $6,600 worth of carpet and flooring generate the following deductions over time | ||||

| Carpet DV | Carpet PC | Floating timber DV | Floating timber PC | |

| 1 Year | $1,650 | $825 | $880 | $440 |

| 2 Year | $1,238 | $825 | $763 | $440 |

| 3 Year | $928 | $825 | $661 | $440 |

| 4 Year | $696 | $825 | $573 | $440 |

| 5 Year | $522 | $825 | $496 | $440 |

| 6 Year | $392 | $825 | $430 | $440 |

| 7 Year | $294 | $825 | $373 | $440 |

| 8 Year | $220 | $825 | $323 | $440 |

| 9 Year | $165 | - | $280 | $440 |

| 10 Year | $124 | - | $243 | $440 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 3. Window Covering curtains and blinds costing $2,550 generate the following deductions over time

| Curtains or blinds | ||||

| Curtains and blinds costing $2,550 generate the following deductions over time | ||||

| Curtains DV | Curtains PC | Blinds DV | Blinds PC | |

| 1 Year | $850 | $425 | $510 | $225 |

| 2 Year | $567 | $425 | $408 | $225 |

| 3 Year | $378 | $425 | $325 | $225 |

| 4 Year | $252 | $425 | $261 | $225 |

| 5 Year | $168 | $425 | $209 | $225 |

| 6 Year | $112 | $425 | $167 | $225 |

| 7 Year | $74 | - | $134 | $225 |

| 8 Year | $50 | - | $107 | $225 |

| 9 Year | $33 | - | $86 | $225 |

| 10 Year | $22 | - | $68 | $225 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 4. Water Tank polyethylene and galvanised water tanks costing $3,150 generate the following deductions over time

| Polyethylene or galvanised water tank | ||||

| Polyethylene and galvanised water tanks costing $3,150 generate the following deductions over time |

||||

| Polyethylene DV | Polyethylene PC | Galvanised DV | Galvanised PC | |

| 1 Year | $420 | $210 | $252 | $126 |

| 2 Year | $364 | $210 | $232 | $126 |

| 3 Year | $315 | $210 | $213 | $126 |

| 4 Year | $273 | $210 | $196 | $126 |

| 5 Year | $237 | $210 | $181 | $126 |

| 6 Year | $205 | $210 | $166 | $126 |

| 7 Year | $178 | $210 | $153 | $126 |

| 8 Year | $154 | $210 | $141 | $126 |

| 9 Year | $134 | $210 | $129 | $126 |

| 10 Year | $116 | $210 | $119 | $126 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

Table 5. Air Conditioning split system and packaged air conditioning units costing $11,400 generate the following deductions over time

| Split system or packaged air conditioning | ||||

| Split system and packaged air conditioning units costing $11,400 generate the following deductions over time |

||||

| Split system DV | Split system PC | Packaged DV | Packaged PC | |

| 1 Year | $2,280 | $1,140 | $1,520 | $760 |

| 2 Year | $1,824 | $1,140 | $1,317 | $760 |

| 3 Year | $1,459 | $1,140 | $1,142 | $760 |

| 4 Year | $1,167 | $1,140 | $989 | $760 |

| 5 Year | $934 | $1,140 | $858 | $760 |

| 6 Year | $747 | $1,140 | $743 | $760 |

| 7 Year | $598 | $1,140 | $644 | $760 |

| 8 Year | $478 | $1,140 | $558 | $760 |

| 9 Year | $383 | $1,140 | $484 | $760 |

| 10 Year | $306 | $1,140 | $419 | $760 |

Diminishing value continues past the effective life period due to calculation methodology that reduces opening value each year. Low value pool has not been employed in calculations.

The assets Lisa decided to install were:

- floating timber floors ($6,600)

- blinds ($2,550)

- a packaged air conditioning unit ($11,400)

- a galvanised steel rainwater tank ($3,150)

Once the renovations on the property were completed, BMT completed the tax depreciation schedule, which detailed available tax deductions using the prime cost and diminishing value methods.

The decision between using diminishing value and prime cost methods also becomes a crucial decision point for investors like Lisa, as each method provides unique benefits tailored to various investment strategies and timeframes.

Below is a breakdown of the depreciation deductions available to Lisa using the two respective methods. For simplicity, we have assumed that Lisa installed the assets on day 1 of the financial year.

Table 6. Deductions using prime cost and diminishing value methods

| Prime cost | Diminishing value | |||||

| New asset | First full FY year deductions | Yr 1-5 Cumulative | Yr 10-14 Cumulative | First full FY year deductions | Yr 1-5 Cumulative | Yr 10-14 Cumulative |

| Floating timber floors | $440 | $2,200 | $2,200 | $880 | $3,373 | $930 |

| Blinds | $255 | $1,275 | $255 | $478 | $2,234 | $44 |

| Packaged A/C | $760 | $3,800 | $3,800 | $1,520 | $5,826 | $1,607 |

| Rainwater tank – galvanised steel | $126 | $630 | $630 | $252 | $1,074 | $507 |

| Total | $1,581 | $6,630 | $6,885 | $3,130 | $12,507 | $3,088 |

Given that the property is central to Lisa's retirement plan, she opted for the prime cost method of depreciation. This choice allows her to claim smaller yet consistent deductions on the assets until their full value has been recovered.

If the property had been a shorter-term investment which Lisa was planning on selling within a few years, she may have chosen the diminishing value method of depreciation. This method will have entitled her to higher depreciation deductions at the start of depreciation schedule, which would then drop each year until the value of the assets run out.

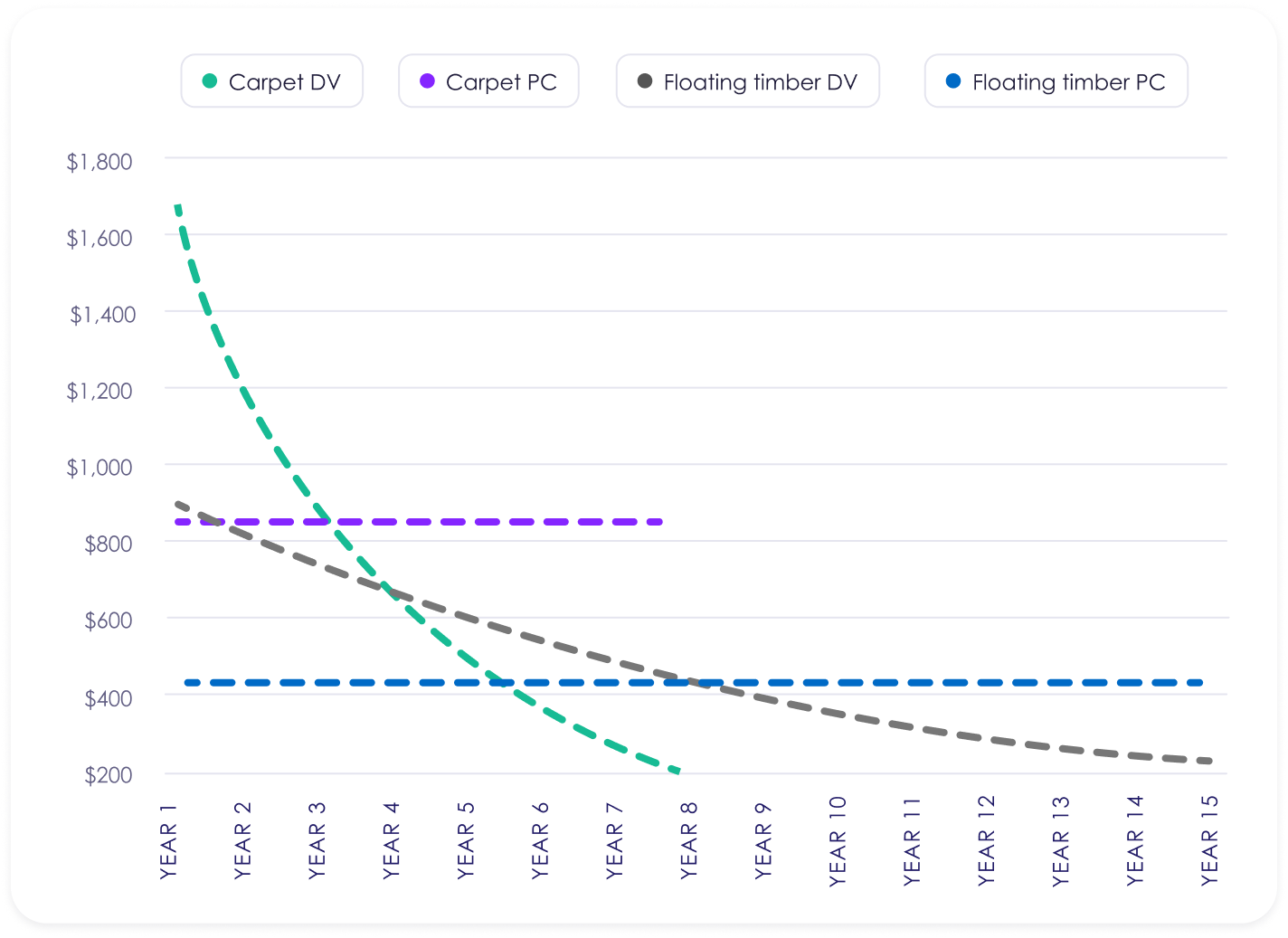

Table 7. This chart illustrates a comparison of depreciation deductions for carpets and floating timber floors using both Diminishing Value and Prime Cost methods.

Both these methods use identical initial asset values, but result in distinct short and long-term deductions, leading to diverse cash flow outcomes to meet the needs of the investor. The allowances that can be claimed are based on the condition, quality, and effective life of each asset.

An investor can only choose one of these depreciation methods for the lifetime of the depreciation schedule which means their choice will be influenced by the investment strategy, income expectations and goals.

As a specialist quantity surveyor, BMT Tax Depreciation will delve into the intricacies of depreciation, helping each client to maximise the returns on their investment while mitigating tax liabilities.

This strategic approach underscores the importance of aligning renovation choices with depreciation goals to optimise cash flow outcomes.

By guiding them towards engaging a quantity surveyor early in the renovation process, accountants can ensure clients make informed decisions that maximise tax benefits while optimising overall financial goals.

A BMT Tax Depreciation Schedule will show both depreciation methods, allowing the investor to determine which method would best suit their goals. Maximise your depreciation deductions by Requesting a Quote.

BMT recommend consulting a financial advisor before making important financial decisions.

Connect with us

Stay up to date

Subscribe to receive the latest

BMT news and announcements.